ABOUT THIS CONTENT

A compiled listing of the most common and useful fiance formulas.

NPV = PVinflows – PVoutflows

IRR = i that makes NPV = 0

UAS – annuity that = PV of irregular cash flow pattern

Ri= realized asset = expected return

ß=1 ⇒ average risk

ß<1 ⇒ below average risk

ß>1 ⇒ above average risk

CAPM relates a security’s relevant risk (ß) to expected return.

CFAT (indirect) = market value of asset sold – tax liability = MV – (MV – BV)(𝜏)

Increase in working capital, ΔWC = CA – CL

ΔCFAT = (ΔS – ΔC – ΔD)(1 – 𝜏) + ΔD {S = sales, C = costs, D = depreciation}

![]()

![]()

NPV (loan) = Amount borrowed – PV (all after-tax payments)

APV (Adjusted PV) = All equity value – PV(FC) + NPV(loan)

- Calculate NPV for all-equity financing

- Adjust NPV for flotation costs

- Adjust NPV for tax shield + subsidization

WACC (weighted average cost of capital)

![]()

{D + E = V}

Pure Play Method

- Find publicly traded company with business similar

- Determine equity beta (ße) for pre-play firm’s stock.

- Calculate pure-play assets ßA

to proposed project.

Loan $ = Gross Proceeds (1 – FC%)

When to Lease?

If there is a tax differential or if the lease lowers transaction costs and/or reduces uncertainty

Lessee (user): 0 = Io – Max[1-𝜏cu] × PVFA[T,rD(1-𝜏cu)] – D × 𝜏cu × PVFA[T,rD(1-𝜏cu)] Lessor (owner): 0 = -Io – Min[1-𝜏co] × PVFA[T,rD(1-𝜏co)] + D × 𝜏co × PVFA[T,rD(1-𝜏co)]

RRRD = Rf + ßD[Rm – Rf]

RRRA = Rf + ßA[Rm – Rf]

ROE = ROA + D/E[ROA – Rf]

ROA = RRREu = Rf + ßA[Rm – Rf] – expected return on an un-levered firm’s assets

RRREl = RRREu + D/E [RRREu – RRRD]

ROA = [E/(D+E)](ROE) + [D/(D+E)](Rf)

ßA = [D/(D+E)]( bD) + [E/(D+E)]( ßE)

ßE = ßA + D/E(ßA – ßD)

E(RE) = Rf + ßE [E(Rm) – Rf] – M&M CAPM (Equity)

Payout Ratio = % Earnings paid as dividends

Retention Ratio = 1 – Payout Ratio

g = (Retention Ratio)(ROE)

ROE = NI/Earnings = Earnings/Book Equity

![]()

PVGO = PV[PV(cash inflows at time t) – PV(cash outflows at time t)] – present value growth option

Valuefirm = Cost of Assets + PV(OCF)

E = VF – D {D = amount borrowed/rD}

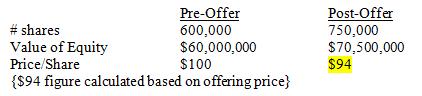

1 share offered for $70 + 4 rights {150,000 new shares offered ⇒ $10,500,000 additional equity}

⇒ 4 rights = $94 – $70 = $24

⇒ 1 right = $6

M&M (Modigliani and Miller)

Proposition 1: method of structuring D/E has no effect on firm value

Proposition 2: cost of equity capital increases as amount of debt increases

Assumes:

- No taxes

- No transaction costs

- No changes in investment policy

Click to Add the First »